Friday, December 21, 2012

Nashville Tennessee Real Estate Investing

Nashville Real Estate Investor - Investment Articles Forum Tips Clubs. Real Estate Investments - Real Estate Investing - Real Estate Market Trends. Real Estate Investing Real estate investing involves residential and commercial rental properties, high rises, real estate investment trusts or REITs, office complexes and more. Whether it's a rental condo or a large office complex, use the tools and resources here to build and manage a profitable real estate investment portfolio. Government Bonds Compared to Real Estate Investment. Top Ways that Real Estate Investment Returns Profits. How Leverage Works Risks of Leverage in Real Estate Investment. Real Estate Investments clear your selections. Related blogs on: real estate investing Everything Real Estate Real estate investing HB Investment Blog Smart Real Estate Investing Add your blog to.

Relocatable Buildings - Product Sites

relocatable buildings - Product Sites

So instead of just wasting time i figured i should start some research for the upcoming projects so i've found a few useful sites with information on relocatable buildings. Hopefully you get some inspiration from them.

Wednesday, November 14, 2012

Modular Buildings In Modern Times

These temporary dwellings have been used by schools, hospitals and churches to create space and save money. Whether these prefabricated buildings cater for a larger congregation, additional class or storage unit, a modular buildings serves many purposes. It was initially intended to be a temporary structure, but many companies specialise in designing structures that last long and are safe.

The process starts with the client consultation when needs and plans are assessed. The constructor will ask the relevant questions and provide some alternative suggestions while sharing professional ideas and plans. The financial quote will be drawn up along with deadlines for construction and the blueprint of the building. Once these terms have been agreed and a contract has been drawn up, the construction of the modular building begins at the factory and most of the work is completed there. This is convenient for the contractor who has tools, labourers and materials in one place and this saves transport costs and inconvenience. The client benefits with less construction noise and mess and this is a beneficial arrangement for both parties.

The days of boiling in a prefab classroom with little ventilation have been replaced by prefab buildings with air conditioning and climate control. The structure is more sturdy, with greater space and stability than before and the architects design according to the client's needs. If you require a darkroom, a modular building can omit all external light and provide the benefits of a darkroom for a fraction of the price.

Modular buildings in the medical industry can be designed to have access control and security features like any high-security laboratory. Modular and relocatable buildings are no longer mass produced identical buildings as each building has unique features according to its use. They are built to last and withstand the elements and be useful to the inhabitants. The building costs are less as modular buildings are built at the factory where all the tools and experts are situated in one place to supervise various projects and this enables the builders to finish more than one construction at one time. It also saves money compared to conventional brick and mortar construction as less money is spent on cement, roofing materials and fittings.

Various Forms Of The Room Of Dreams.

We are composed of various rooms. When we started to build a House, it will take a long time to complete as many of the space. But now we provide you, ready to be used in space relocatable buildings. You can choose from a variety of models that we offer. Please contact us for your convenience to have the home of your dreams.

Saturday, November 10, 2012

Uncategorized Websites Web Design CSS3 Photography Tutorials Wordpress Plugins Trending: Bloggermint Blogger Template Sell Your House Fast Even in a Buyers Market

sell your house fast Do you want to sell your house fast? Do you need to sell your house fast? Whether you simply want to avoid a bunch of hassle when you decide to sell or have fallen into economic circumstances that are forcing you to sell, there are options available to you that can help you sell your house fast.

There are now dozens or companies that understand what you need and can help you get out from under your mortgage payments with a quick purchase. Generally, these companies are made up of one or more real estate investors who can afford to hold onto a piece of property for a while to sell it later, fix it up for resale, or change the zoning of the property to use it for another purpose.

If you really want to sell your house fast, one of these home-buying organizations can probably help you. Most offer cash purchases without any fees to sellers, even if your house is in need of repairs. And most can buy within a few days to a couple of weeks if need be.

You may have to settle for a lower price than you might otherwise get; after all, these are investors who offer the convenience of allowing you to sell your house fast in exchange for the opportunity to make a profit on your home after a refurbish or repairs are made. This really shouldn't be an option for you. There's no shame in wanting to sell your house quickly and wanting top dollar.

Of course, you could seek the assistance of a professional. There's nothing wrong with working with someone that will list your house for you. Because we are in a rather slow real estate market, this is not the best time to try to sell your house yourself. But don't let that stop you. A professional realtor will be able to help you properly price your home, bring in potential buyers, show you how to optimize the appearance and staging of your home so it is appealing to buyers, and market your property for you.

On top of using a realtor you should also use unconventional methods to sell your home. After all the traditional way of listing and selling your home is set up for a sellers market. Since you are in a buyers market you need to get involved and think out of the box a little bit if you want to sell your house fast.

Monday, November 5, 2012

Wednesday, October 17, 2012

Weak Recovery Denial

Paul Krugman disagrees with my recent post that the recovery is weak compared to recoveries from past serious U.S. recessions including those associated with financial crises. I’ve been writing about the reasons for weak recovery for two years, but the issue has heated up because of its relevance to the elections this fall.

In making his critique, Krugman appeals to a recent oped in Bloomberg View by Carmen Reinhart and Ken Rogoff who criticize the research of economic historian Michael Bordo and his coauthor Joseph Haubrich of the Cleveland Fed, which I have referred to. Bordo and Haubrich demonstrate that the recovery from the recent recession and financial crisis has been unusually weak compared to recoveries from past recessions with financial crises in the United States. In separate research, Jerry Dwyer and Jim Lothian report the same finding. Neither Reinhart-Rogoff nor Krugman disprove this finding.

To see this, consider the points made by Reinhart and Rogoff, and also by Krugman.

First, they argue for a narrower definition of a financial crisis. Reinhart and Rogoff say that one should “distinguish systemic financial crises from more minor ones and from regular business cycles.” Thus they exclude some cases studied by Bordo and Haubrich. But narrowing the focus to systemic crises in this way does not change the Bordo-Haubrich findings because the recovery from the recent recession is weaker than the average of past recessions cum financial crises even with these exclusions.

Second, Reinhart and Rogoff argue that one should look at recessions together with recoveries when looking at severity. In fact, in their work they explicitly “don’t delineate between the ‘recession’ period and the ‘recovery’ period.” But there is no disagreement that recessions associated with financial crises have tended to be deeper than those without financial crises. I certainly don’t deny that there was a serious financial crisis. In fact I wrote one of the first books on the crisis and found that government policy prior to 2009 was to blame, just as government policy was to blame for the even more serious Great Depression.

The issue that I and others have focused on is whether the recovery is unusually weak. By mixing recessions with recoveries Reinhart and Rogoff blur the classic distinction, which has long been at the heart of macroeconomic analysis. Because they do not examine recoveries per se, their empirical analysis does not disprove the fact that the current recovery is very weak as Bordo and Haubrich and others have shown.

Third, there is the complaint that in a simple chart I used to show how weak the recovery has been, I only looked at the first four quarters of recovery. But I also mentioned that Bordo and Haubrich use a different measure, which goes well beyond 4 quarters, and come to the same conclusion, and also that the current recovery has weakened further since the first four quarters. In any case, the focus on four quarters has nothing to do with it. Here is a chart that looks at growth during the first eight quarters. The story is the same.

Since most of the Reinhart, Rogoff and Krugman criticism is implicitly aimed at the historical work of Bordo and Haubrich, it is appropriate to conclude with what Bordo wrote in response to a press inquiry which he shared with me. Bordo puts it this way:

Since most of the Reinhart, Rogoff and Krugman criticism is implicitly aimed at the historical work of Bordo and Haubrich, it is appropriate to conclude with what Bordo wrote in response to a press inquiry which he shared with me. Bordo puts it this way:

Aside from the unnecessary political rhetoric and ad hominems, the basic difference between my research with Joseph Haubrich on U.S. recoveries and that of Carmen Reinhart and Ken Rogoff is over the methodology of defining a recovery. Reinhart and Rogoff focus on the behavior of the level of real per capita GDP from the peak preceding the financial crisis to the point in the succeeding recovery at which the earlier peak level of real per capita GDP is reached. We look at what is called the bounce back, the pace of recovery from the trough of the business cycle.

We find that deep recessions accompanied by financial crises bounce back faster than recessions which do not have financial crises. These results are even stronger when we focus on what Reinhart and Rogoff call systemic crises, like 1893 and 1907. The recent recession and financial crisis is a major exception to this pattern. The recovery remains tepid after three years.

Reinhart and Rogoff s methodology combines the downturn with the recovery. Using our data but following their approach one would get the same results as they do, that recessions with financial crises have slow recoveries as I show in my Wall Street Journal op ed. Their use of real per capita GDP rather than just real GDP would not make any difference to our results. Thus comparing their methodology with ours is like comparing apples with oranges. Our approach focuses directly on the question-- are recoveries after recessions with financial crises associated with slower or faster than average recoveries. Their approach answers a different question than we ask.

In sum, the weak recovery deniers have not made their case.

In making his critique, Krugman appeals to a recent oped in Bloomberg View by Carmen Reinhart and Ken Rogoff who criticize the research of economic historian Michael Bordo and his coauthor Joseph Haubrich of the Cleveland Fed, which I have referred to. Bordo and Haubrich demonstrate that the recovery from the recent recession and financial crisis has been unusually weak compared to recoveries from past recessions with financial crises in the United States. In separate research, Jerry Dwyer and Jim Lothian report the same finding. Neither Reinhart-Rogoff nor Krugman disprove this finding.

To see this, consider the points made by Reinhart and Rogoff, and also by Krugman.

First, they argue for a narrower definition of a financial crisis. Reinhart and Rogoff say that one should “distinguish systemic financial crises from more minor ones and from regular business cycles.” Thus they exclude some cases studied by Bordo and Haubrich. But narrowing the focus to systemic crises in this way does not change the Bordo-Haubrich findings because the recovery from the recent recession is weaker than the average of past recessions cum financial crises even with these exclusions.

Second, Reinhart and Rogoff argue that one should look at recessions together with recoveries when looking at severity. In fact, in their work they explicitly “don’t delineate between the ‘recession’ period and the ‘recovery’ period.” But there is no disagreement that recessions associated with financial crises have tended to be deeper than those without financial crises. I certainly don’t deny that there was a serious financial crisis. In fact I wrote one of the first books on the crisis and found that government policy prior to 2009 was to blame, just as government policy was to blame for the even more serious Great Depression.

The issue that I and others have focused on is whether the recovery is unusually weak. By mixing recessions with recoveries Reinhart and Rogoff blur the classic distinction, which has long been at the heart of macroeconomic analysis. Because they do not examine recoveries per se, their empirical analysis does not disprove the fact that the current recovery is very weak as Bordo and Haubrich and others have shown.

Third, there is the complaint that in a simple chart I used to show how weak the recovery has been, I only looked at the first four quarters of recovery. But I also mentioned that Bordo and Haubrich use a different measure, which goes well beyond 4 quarters, and come to the same conclusion, and also that the current recovery has weakened further since the first four quarters. In any case, the focus on four quarters has nothing to do with it. Here is a chart that looks at growth during the first eight quarters. The story is the same.

Aside from the unnecessary political rhetoric and ad hominems, the basic difference between my research with Joseph Haubrich on U.S. recoveries and that of Carmen Reinhart and Ken Rogoff is over the methodology of defining a recovery. Reinhart and Rogoff focus on the behavior of the level of real per capita GDP from the peak preceding the financial crisis to the point in the succeeding recovery at which the earlier peak level of real per capita GDP is reached. We look at what is called the bounce back, the pace of recovery from the trough of the business cycle.

We find that deep recessions accompanied by financial crises bounce back faster than recessions which do not have financial crises. These results are even stronger when we focus on what Reinhart and Rogoff call systemic crises, like 1893 and 1907. The recent recession and financial crisis is a major exception to this pattern. The recovery remains tepid after three years.

Reinhart and Rogoff s methodology combines the downturn with the recovery. Using our data but following their approach one would get the same results as they do, that recessions with financial crises have slow recoveries as I show in my Wall Street Journal op ed. Their use of real per capita GDP rather than just real GDP would not make any difference to our results. Thus comparing their methodology with ours is like comparing apples with oranges. Our approach focuses directly on the question-- are recoveries after recessions with financial crises associated with slower or faster than average recoveries. Their approach answers a different question than we ask.

In sum, the weak recovery deniers have not made their case.

Monday, October 15, 2012

More on the Unusually Weak Recovery

The weak recovery continues to be a major topic. Over the weekend, Russ Roberts issued the second episode of his three part “chartcast” series on the topic, which is based on interviews with me and builds on his highly-regarded podcast series, but with helpful charts and illustrations. (Here is the first episode). Among other things we discuss the work of Mike Bordo and Joe Haubrich on the unusual nature of this recovery, and their views of the work by Carmen Reinhart and Ken Rogoff.

Also, as Jon Hilsenrath and Ezra Klein report, over the weekend Carmen Reinhart and Ken Rogoff released a short rebuttal to Bordo and Haubrich as well as to several opeds. Reinhart and Rogoff argue in favor of a narrower definition of a financial crisis, and they thus focus on a subset of the eight Bordo-Haubrich recessions with financial crises (for example, they exclude 1913 and 1982). This alone does not change the Bordo-Haubrich results as the figure in my post of last week makes clear. But Reinhart and Rogoff argue that one should look at the downturn as well as the recovery when looking at severity. There is no disagreement that recessions associated with financial crises have tended to be deeper than those without financial crises. The disagreement is over the recoveries. By mixing downturns with recoveries Reinhart and Rogoff get different results from Bordo and Haubrich.

But the question for policy now is whether the recovery has been unusually slow compared to earlier recoveries from recessions with financial crises, and the evidence is still clear that it has been. Papers in the book Government Policies and the Delayed Economic Recovery edited by Lee Ohanian, Ian Wright, and me show that policy is the reason.

Also, as Jon Hilsenrath and Ezra Klein report, over the weekend Carmen Reinhart and Ken Rogoff released a short rebuttal to Bordo and Haubrich as well as to several opeds. Reinhart and Rogoff argue in favor of a narrower definition of a financial crisis, and they thus focus on a subset of the eight Bordo-Haubrich recessions with financial crises (for example, they exclude 1913 and 1982). This alone does not change the Bordo-Haubrich results as the figure in my post of last week makes clear. But Reinhart and Rogoff argue that one should look at the downturn as well as the recovery when looking at severity. There is no disagreement that recessions associated with financial crises have tended to be deeper than those without financial crises. The disagreement is over the recoveries. By mixing downturns with recoveries Reinhart and Rogoff get different results from Bordo and Haubrich.

But the question for policy now is whether the recovery has been unusually slow compared to earlier recoveries from recessions with financial crises, and the evidence is still clear that it has been. Papers in the book Government Policies and the Delayed Economic Recovery edited by Lee Ohanian, Ian Wright, and me show that policy is the reason.

Saturday, October 13, 2012

Getting Tax Reform History Right

"For the past 75 years or so, tax reform has been defined by a tradeoff: broaden the tax base and lower rates,” as tax historian Joseph Thorndike explained in a recent article. That’s the framework behind the Romney tax reform proposal, as well as the last major federal tax reform in 1986. History tells us that such a strategy will work if the tradeoff and its pro-growth purpose are explained to the American people, and the mechanics of base expansion are then worked out in bipartisan negotiations with Congress. That’s the lesson from the 1986 tax reform in which Ronald Reagan put forth the general framework and the details were then negotiated with Democrats and Republicans in Congress. That history lesson is very important now, but it will be lost if Americans don’t get the history right.

That is why my colleague and tax expert Charlie McLure was so concerned when he heard Vice-President Biden describe President Reagan’s approach to the 1986 tax reform in the vice-presidential debate this week. Charlie served in the U.S. Treasury in the 1980s and was responsible for preparing the tax proposals for President Reagan. As Charlie explained in an email yesterday, the history told in the debate wasn’t right:

"During the Vice-Presidential debate, Vice-President Joe Biden asserted that President Ronald Reagan made his tax reform proposals public. The implication – and the only context in which the assertion would be relevant – is that he did so during the 1984 Presidential campaign. This is not true. As Deputy Assistant Secretary of the Treasury, I was responsible for preparation of the Treasury Department’s proposals to President Reagan. In his 1984 State of the Union address, President Reagan gave Treasury Secretary Don Regan the mandate to send him the proposals by a date in November that fell after the election. That is what we did. The President did not endorse the Department’s proposals and did not send his proposals to the Congress until May 1985, six months after the election. Had he done that before the election, the resulting demagoguery would have forced him to take so many options off the table that the Tax Reform Act of 1986 would not have happened – or at least would not have been the landmark legislation that it was."

That is why my colleague and tax expert Charlie McLure was so concerned when he heard Vice-President Biden describe President Reagan’s approach to the 1986 tax reform in the vice-presidential debate this week. Charlie served in the U.S. Treasury in the 1980s and was responsible for preparing the tax proposals for President Reagan. As Charlie explained in an email yesterday, the history told in the debate wasn’t right:

"During the Vice-Presidential debate, Vice-President Joe Biden asserted that President Ronald Reagan made his tax reform proposals public. The implication – and the only context in which the assertion would be relevant – is that he did so during the 1984 Presidential campaign. This is not true. As Deputy Assistant Secretary of the Treasury, I was responsible for preparation of the Treasury Department’s proposals to President Reagan. In his 1984 State of the Union address, President Reagan gave Treasury Secretary Don Regan the mandate to send him the proposals by a date in November that fell after the election. That is what we did. The President did not endorse the Department’s proposals and did not send his proposals to the Congress until May 1985, six months after the election. Had he done that before the election, the resulting demagoguery would have forced him to take so many options off the table that the Tax Reform Act of 1986 would not have happened – or at least would not have been the landmark legislation that it was."

Thursday, October 11, 2012

Simple Proof That Strong Growth Has Typically Followed Financial Crises

People are looking for answers to why the economy is growing so slowly. Is the answer that economic growth is normally weak following deep recessions and financial crises, as, for example, Kenneth Arrow argued in the presidential election event with me this week at Stanford? Or is poor economic policy the answer, as I argued?

The bars show the growth rate in the first four quarters following all previous American recessions that are associated with financial crises, as identified by Bordo and Haubrich. The upper line shows the average growth rate in all those recoveries. The lower line shows the growth rate in the four quarters following the 2007-2009 recession. It is very clear that recessions with financial crises are normally followed by much more rapid recoveries than this current recovery. The current recovery not only started out weak, averaging 2.5% in the first year, it got weaker over time, declining to only 1.3% in the second quarter of this year.

Growth was nearly 4 times stronger on average in the past recoveries. The only recovery in this list in which growth was as weak as this one followed the 1990-91 recession, but that was from a very shallow recession with output declining only 1.1%, so growth did not need to get very high to catch up. (The chart would look very similar if instead of 4 quarters you use the length of the recession from peak to trough as Bordo and Haubrich also do).

With such obvious evidence, how can people come to different views? Usually they mix in experiences in other countries with different economies at different points in time, as for example Carmen Reinhart and Kenneth Rogoff have done in an often cited book. But this approach can lead to mistaken conclusions, as Bordo explained recently in the Wall Street Journal. As he put it, “The mistaken view comes largely from the 2009 book "This Time Is Different," by economists Carmen Reinhart and Kenneth Rogoff, and other studies based on the experience of several countries in recent decades. The problem with these studies is that they lump together countries with diverse institutions, financial structures and economic policies.”

In my view the facts contradict the “deep recession cum financial crisis” answer, so I have focused my research on economic policy and have found that the answer lies there. The chart below illustrates these facts. It is derived from historical data reported in a paper by economic historians Michael Bordo of Rutgers and Joe Haubrich at the Cleveland Fed.

Growth was nearly 4 times stronger on average in the past recoveries. The only recovery in this list in which growth was as weak as this one followed the 1990-91 recession, but that was from a very shallow recession with output declining only 1.1%, so growth did not need to get very high to catch up. (The chart would look very similar if instead of 4 quarters you use the length of the recession from peak to trough as Bordo and Haubrich also do).

With such obvious evidence, how can people come to different views? Usually they mix in experiences in other countries with different economies at different points in time, as for example Carmen Reinhart and Kenneth Rogoff have done in an often cited book. But this approach can lead to mistaken conclusions, as Bordo explained recently in the Wall Street Journal. As he put it, “The mistaken view comes largely from the 2009 book "This Time Is Different," by economists Carmen Reinhart and Kenneth Rogoff, and other studies based on the experience of several countries in recent decades. The problem with these studies is that they lump together countries with diverse institutions, financial structures and economic policies.”

Monday, October 8, 2012

Recent Part-time Job Increase Is Not a Good Sign

Many have noted the large September increase in “part-time employment for economic reasons” reported in the BLS household survey. The 582,000 increase in these part time jobs caused total employment to rise by 873,000—a major reason for the decrease of the overall unemployment rate, and the broader U-6 measure of labor underutilization—which adds in this part-time employment—did not decline at all.

This increase in part time jobs is not a good sign for the economy.

Joe LaVorgna, chief US economist at Deutsche Bank, argues that the part-time increase is likely due to the election. He offers two pieces of evidence. First, there was an unusually large gain in non-private employment, defined as total employment less “private industries” employment, which thus includes campaign workers who organize grass roots efforts, make phone calls, knock on doors, or help at political conventions. Second, there was an unusually large increase in employment in the 20 to 24 year age group—a typical age for campaign workers. The explanation is appealing because both Democrats and Republicans are increasing such grass roots campaigns. State data—especially from the swing states—is needed to confirm LaVorgna’s hypothesis. But if true the increase in part time employment is not a sign of an improving economy: it implies that the jobs gain in September is largely temporary.

Another view is that the increase in part-time employment is directly due to the weak recovery, and a sign that it is getting weaker. Surges in part time employment frequently occur in times of economic stress. Consider, for example, all the months in which part time employment rose by 500,000 or more. There are 13 such monthly increases in the BLS data base—Jan 1958, Mar 1958, Jan 1975, May 1980, Oct 1981, Feb 1982, Feb 1991, Sep 2001, Nov 2008, Dec 2008, Feb 2009, Sep 2010, Sep 2012. With two exceptions, every one of these occurred during recessions when the economy was sharply contracting. The two exceptions are in the current recovery, which ia another measure of its weakness.

Even more troublesome is that in the past 6 months of the recovery, the entire employment increase was more than accounted for by part time jobs: Total employment rose by 940,000 from March to September and part time employment rose by 941,000. This deterioration in the labor market is consistent with the dip in economic growth to 1.3 percent in the 2nd quarter. It too is not a sign that the economy is improving.

This increase in part time jobs is not a good sign for the economy.

Joe LaVorgna, chief US economist at Deutsche Bank, argues that the part-time increase is likely due to the election. He offers two pieces of evidence. First, there was an unusually large gain in non-private employment, defined as total employment less “private industries” employment, which thus includes campaign workers who organize grass roots efforts, make phone calls, knock on doors, or help at political conventions. Second, there was an unusually large increase in employment in the 20 to 24 year age group—a typical age for campaign workers. The explanation is appealing because both Democrats and Republicans are increasing such grass roots campaigns. State data—especially from the swing states—is needed to confirm LaVorgna’s hypothesis. But if true the increase in part time employment is not a sign of an improving economy: it implies that the jobs gain in September is largely temporary.

Another view is that the increase in part-time employment is directly due to the weak recovery, and a sign that it is getting weaker. Surges in part time employment frequently occur in times of economic stress. Consider, for example, all the months in which part time employment rose by 500,000 or more. There are 13 such monthly increases in the BLS data base—Jan 1958, Mar 1958, Jan 1975, May 1980, Oct 1981, Feb 1982, Feb 1991, Sep 2001, Nov 2008, Dec 2008, Feb 2009, Sep 2010, Sep 2012. With two exceptions, every one of these occurred during recessions when the economy was sharply contracting. The two exceptions are in the current recovery, which ia another measure of its weakness.

Even more troublesome is that in the past 6 months of the recovery, the entire employment increase was more than accounted for by part time jobs: Total employment rose by 940,000 from March to September and part time employment rose by 941,000. This deterioration in the labor market is consistent with the dip in economic growth to 1.3 percent in the 2nd quarter. It too is not a sign that the economy is improving.

Sunday, October 7, 2012

From Economic Scare Stories to the Other Side of Reality

Twenty years ago this month my colleague Bob Hall and I wrote an op-ed for the New York Times about how “in recent months press reporting about the economy has become so pessimistic that it has completely lost touch with reality.” (October 16, 1992). The Times editors headlined our article “Economic Scare Stories,” which captured our point perfectly and fit the Halloween season. In October 1992, economic growth was improving following the 1990-91 recession, but most reporting looked beyond good economic news and said that the economy was doing poorly. Amazingly, the frequently-reported view that the economy in October 1992 was like the Great Depression went unchallenged. So we challenged it, hoping that our article would in some small way result in improved reporting.

Today press reporting seems to have switched to the other side of reality. Compared to October 1992, economic growth is now slower, unemployment is higher, and tragically the long-term unemployment rate is twice has high. And reported economic growth has been declining rather than improving as it was in 1992. Yet, in recent months much reporting about the economy has turned so upbeat that it has again lost touch with reality. Many look beyond the tragic growth or employment news and say that the economy is improving, or that things could have been worse, emphasizing that it is fortunately nothing like the Great Depression.

When asked what caused the switch, I answer, facetiously, that people must have read our article, remembered it, tried to make a correction, but unintentionally overcorrected. That answer, of course, is out of touch with the reality that both October 1992 and October 2012 constitute the final days of a presidential election where the main issue is the economy, and, as Bob Hall and I wrote, “people’s perceptions about the economy affect elections.”

Today press reporting seems to have switched to the other side of reality. Compared to October 1992, economic growth is now slower, unemployment is higher, and tragically the long-term unemployment rate is twice has high. And reported economic growth has been declining rather than improving as it was in 1992. Yet, in recent months much reporting about the economy has turned so upbeat that it has again lost touch with reality. Many look beyond the tragic growth or employment news and say that the economy is improving, or that things could have been worse, emphasizing that it is fortunately nothing like the Great Depression.

When asked what caused the switch, I answer, facetiously, that people must have read our article, remembered it, tried to make a correction, but unintentionally overcorrected. That answer, of course, is out of touch with the reality that both October 1992 and October 2012 constitute the final days of a presidential election where the main issue is the economy, and, as Bob Hall and I wrote, “people’s perceptions about the economy affect elections.”

Friday, September 21, 2012

Regulatory Expansion Versus Economic Expansion in Two Recoveries

Much can be learned by comparing the very weak recovery from the 2007-2009 recession with the very strong recovery from the 1981-82 recession. Both recessions were severe, and U.S. history shows that severe recessions tend to be followed by fast recoveries, even when the severe recession is due to a financial crisis. But growth has averaged only 2.2 percent in this recovery while it averaged 5.7 percent in the 1980s recovery as shown in this chart.

As I testified in a House Judiciary Committee hearing on regulation yesterday, I’ve come to the conclusion that the difference between the two recoveries is due a difference in government policies, including regulatory policy.

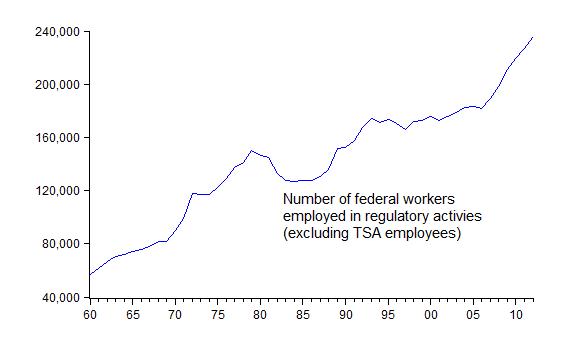

One measure of the difference between the regulatory policies in the two recoveries is shown in the next chart. It compares the number of federal workers engaged in regulatory activities in the years before and during both recoveries. Note that in the early 1980s the number of federal workers in these regulatory areas was declining, in sharp contrast to the situation now, even when TSA workers are excluded as in this chart.

While correlation does not prove causation, regulations, whatever their benefits, tend to raise the cost of doing business and thus discourage business expansion and economic growth. This does not imply that increased regulation was the cause of the recession, which was surely due to other factors including financial and monetary shocks. But had legislation been passed into law to contain the recent regulatory expansion, it is likely that we would have had a stronger economic recovery.

The data on federal workers comes from this paper by Susan Dudley and Melissa Warren. This chart shows the full series going back to the 1960s, again adjusted for TSA workers in recent years.

Wednesday, September 19, 2012

The Eroding Effect of QE3 on Mortgage Spreads

It has been a week now since the Fed’s QE3 announcement that it would be again buying mortgage backed securities (MBS). There was an initial decline in the mortgage spread on the announcement but, as often happens, that initial impact seems to have been eroding away day by day.

Take a look at this Bloomberg chart of the option adjusted spread (OAS) for mortgage securities. Wednesday September 12 is marked so you can see the effect on Thursday September 13 when the Fed made the announcement. The spread moved down again on Friday, but this week it went back up. By Wednesday September 19 it had completely returned to the pre-announcement value. The effect on the spread has eroded away.

One should also note that the effect on mortgage rates depends on what happens to other rates, such as Treasury yields, as well as the spread. But the yield on 10-year Treasuries has risen since QE3. So in effct, the overall effect on mortgage rates could even end up being counter to the Fed's intentions in the end.

Take a look at this Bloomberg chart of the option adjusted spread (OAS) for mortgage securities. Wednesday September 12 is marked so you can see the effect on Thursday September 13 when the Fed made the announcement. The spread moved down again on Friday, but this week it went back up. By Wednesday September 19 it had completely returned to the pre-announcement value. The effect on the spread has eroded away.

Of course, the effect of the announcement could already have been discounted before September 13, in which case some of the earlier downward movements could be attributed to QE3. Nonetheless, this real time experience is a good illustration of why announcement day measures—which the Fed has relied on to assess its LSAP programs—can be misleading. This is why Johannes Stroebel and I used other techniques in our analysis of the earlier MBS program, in which we did not find significant effects.

Friday, September 7, 2012

A New Chart Cast on the Bad News Recovery

As many have observed the employment report for August released today was disappointing news, but it really is a continuation of a steady stream of bad employment news that has been the story of this recovery since its beginning. The economy is growing too slowly to increase jobs at a pace that matches the growing population—unlike previous recoveries from deep recessions.

Here is an update of the chart that compares the change in the employment to population ratio in this recovery with the recovery from the deep slump of the early 1980s. This percentage dropped a litttle in August, but the big story is that there has never been a lift off.

Russ Roberts has produced a fascinating a new "chartcast" which illustrates how unusually poor this recovery has been. Through a series of questions and answers he traces through several key charts with me. It is a visual version of his very successful podcast series Econ Talk.

Russ is planning a follow-up chartcast which gets into the causes of the slow recovery.

Tuesday, September 4, 2012

Strong Push Back at Jackson Hole

In his Jackson Hole speech, Ben Bernanke argued that quantitative easing (in particular Large Scale Asset Purchases, or LSAPs) has had large macroeconomic effects, saying that “a study using the Board’s FRB/US model of the economy found that, as of 2012, the first two rounds of LSAPs may have raised the level of output by almost 3 percent and increased private payroll employment by more than 2 million jobs, relative to what otherwise would have occurred.” He footnoted a Fed paper by Hess Chung et al, in which the authors plugged in other people’s estimates of the impact of LSAPs on long term rates into the FRB/US model which does not have its own estimates.

However, a number of conference participants pushed back on this view, including John Ryding of RDQ, Mickey Levy of Bank of American and me, but most of all Michael Woodford whose paper showed in detail how empirical evidence and basic economic theory did not support these beneficial effects.

Woodford’s empirical evidence included a simple graph (Fig 15) showing that there was no economic growth effect around the times of the expansions in the size of the Fed’s balance and thus that the quantitative easing had “little evident effect on aggregate nominal expenditure…”

He challenged the view that the LSAPs lowered long term rates or at least had the kind of impact assumed by Chung et al. He explained that “‘portfolio-balance effects’ do not exist in a modern, general-equilibrium theory of asset prices…” which is what many of us have been teaching students for thirty years.

He questioned the various event studies cited by the Fed, such as Gagnon et al, saying "it is not clear that their announcement-days-only measure should be regarded as correct."

He showed that the often-cited evidence reported by Arvind Krishnamurthy and Annette Vissing-Jorgensen that “purchases of long-term Treasuries could raise the price of (and so lower the yield on) Treasuries…would not necessarily imply any reduction in other long-term interest rates, since the increase in the price of Treasuries would reflect an increase in the safety premium, and not necessarily any increase in their price apart from the safety premium…This means that while the US Treasury would then be able to finance itself more cheaply at the margin, there would not necessarily be any such benefit for private borrowers, and hence any stimulus to aggregate expenditure….There seems little reason to believe that purchases of long-term Treasuries should be an effective way of lowering the kind of longer-term interest rates that matter most for stimulating economic activity.”

Woodford also questioned the beneficial impacts of forward guidance as practiced by the Fed so far, saying that “simply presenting a forecast that the policy rate will remain lower for longer than had previously been expected, in the absence of any reason to believe that future policy decisions will be made in a different way, runs the risk of being interpreted as simply an announcement that the future is likely to involve lower real income growth and/or lower inflation than had previously been anticipated — information that, if believed, should have a contractionary rather than an expansionary effect.”

In Woodford’s view, forward guidance could have achieved positive effects if it had “made it clear that short-term interest rates will not immediately be increased as soon as a Taylor rule descriptive of past FOMC behavior would justify a funds rate above 25 basis points,” because “this would provide a reason for market participants to expect easier future monetary and financial conditions than they may currently be anticipating, and that should both ease current financial conditions and provide an incentive for increased spending.”

Many Fed watchers interpreted the benefit-cost analysis in Ben Bernanke’s speech as signaling more quantitative easing. But viewed in the context of the whole Jackson Hole meeting, which many FOMC members attended, the benefits are considerably smaller than stated in that speech, and perhaps even negative.

However, a number of conference participants pushed back on this view, including John Ryding of RDQ, Mickey Levy of Bank of American and me, but most of all Michael Woodford whose paper showed in detail how empirical evidence and basic economic theory did not support these beneficial effects.

Woodford’s empirical evidence included a simple graph (Fig 15) showing that there was no economic growth effect around the times of the expansions in the size of the Fed’s balance and thus that the quantitative easing had “little evident effect on aggregate nominal expenditure…”

He challenged the view that the LSAPs lowered long term rates or at least had the kind of impact assumed by Chung et al. He explained that “‘portfolio-balance effects’ do not exist in a modern, general-equilibrium theory of asset prices…” which is what many of us have been teaching students for thirty years.

He questioned the various event studies cited by the Fed, such as Gagnon et al, saying "it is not clear that their announcement-days-only measure should be regarded as correct."

He showed that the often-cited evidence reported by Arvind Krishnamurthy and Annette Vissing-Jorgensen that “purchases of long-term Treasuries could raise the price of (and so lower the yield on) Treasuries…would not necessarily imply any reduction in other long-term interest rates, since the increase in the price of Treasuries would reflect an increase in the safety premium, and not necessarily any increase in their price apart from the safety premium…This means that while the US Treasury would then be able to finance itself more cheaply at the margin, there would not necessarily be any such benefit for private borrowers, and hence any stimulus to aggregate expenditure….There seems little reason to believe that purchases of long-term Treasuries should be an effective way of lowering the kind of longer-term interest rates that matter most for stimulating economic activity.”

Woodford also questioned the beneficial impacts of forward guidance as practiced by the Fed so far, saying that “simply presenting a forecast that the policy rate will remain lower for longer than had previously been expected, in the absence of any reason to believe that future policy decisions will be made in a different way, runs the risk of being interpreted as simply an announcement that the future is likely to involve lower real income growth and/or lower inflation than had previously been anticipated — information that, if believed, should have a contractionary rather than an expansionary effect.”

In Woodford’s view, forward guidance could have achieved positive effects if it had “made it clear that short-term interest rates will not immediately be increased as soon as a Taylor rule descriptive of past FOMC behavior would justify a funds rate above 25 basis points,” because “this would provide a reason for market participants to expect easier future monetary and financial conditions than they may currently be anticipating, and that should both ease current financial conditions and provide an incentive for increased spending.”

Many Fed watchers interpreted the benefit-cost analysis in Ben Bernanke’s speech as signaling more quantitative easing. But viewed in the context of the whole Jackson Hole meeting, which many FOMC members attended, the benefits are considerably smaller than stated in that speech, and perhaps even negative.

Wednesday, August 29, 2012

Government Policies and the Delayed Economic Recovery

A year ago, when the economic recovery had already been delayed two years, Lee Ohanain and I got the idea for a book on the role policy in the delay. To make the idea operational we invited people who were working on the topic to a conference and to write chapters. The book Government Policies and the Delayed Economic Recovery is now available as an ebook with printed copies on their way to Amazon and other booksellers.With yet another year of delayed recovery and growing debates about the cause, the topic is more relevant than ever.

Here is how Lee Ohanian, Ian Wright and I summarized the papers and their implications in the Introduction:

The contributors to this book consider a wide range of topics and policy issues related to the delayed economic recovery. While their opinions are not always the same, together they reveal a common theme: the delayed recovery has been due to the enactment of poor economic policies and the failure to implement good economic policies. The discussion at the conference where some of the papers were presented—summarized by Ian Wright—reveals a similar theme.

The clear implication is that a change in the direction of economic policy is sorely needed. Simply waiting for economic problems to work themselves out, hoping that growth will improve as the Great Recession of fades into the distant past, will not be enough to restore strong economic growth in America.

And here is the Table of Contents:

Economic Strength and American Leadership

George P. Shultz

Uncertainty Unbundled: The Metrics of Activism

Alan Greenspan

Has Economic Policy Uncertainty Hampered the Recovery?

Scott R. Baker, Nicholas Bloom, and Steven J. Davis

How the Financial Crisis Caused Persistent Unemployment

Robert E. Hall

What the Government Purchases Multiplier Actually Multiplied in the 2009 Stimulus Package

John F. Cogan and John B. Taylor

The Great Recession and Delayed Economic Recovery: A Labor Productivity Puzzle?

Ellen R. McGrattan and Edward C. Prescott

Why the U.S. Economy Has Failed to Recover and What Policies Will Promote Growth

Kyle F. Herkenhoff and Lee E. Ohanian

Restoring Sound Economic Policy: Three Views

Alan Greenspan, George P. Shultz, and John H. Cochrane

Summary of the Commentary

Ian J. Wright

Here is how Lee Ohanian, Ian Wright and I summarized the papers and their implications in the Introduction:

The contributors to this book consider a wide range of topics and policy issues related to the delayed economic recovery. While their opinions are not always the same, together they reveal a common theme: the delayed recovery has been due to the enactment of poor economic policies and the failure to implement good economic policies. The discussion at the conference where some of the papers were presented—summarized by Ian Wright—reveals a similar theme.

The clear implication is that a change in the direction of economic policy is sorely needed. Simply waiting for economic problems to work themselves out, hoping that growth will improve as the Great Recession of fades into the distant past, will not be enough to restore strong economic growth in America.

And here is the Table of Contents:

Economic Strength and American Leadership

George P. Shultz

Uncertainty Unbundled: The Metrics of Activism

Alan Greenspan

Has Economic Policy Uncertainty Hampered the Recovery?

Scott R. Baker, Nicholas Bloom, and Steven J. Davis

How the Financial Crisis Caused Persistent Unemployment

Robert E. Hall

What the Government Purchases Multiplier Actually Multiplied in the 2009 Stimulus Package

John F. Cogan and John B. Taylor

The Great Recession and Delayed Economic Recovery: A Labor Productivity Puzzle?

Ellen R. McGrattan and Edward C. Prescott

Why the U.S. Economy Has Failed to Recover and What Policies Will Promote Growth

Kyle F. Herkenhoff and Lee E. Ohanian

Restoring Sound Economic Policy: Three Views

Alan Greenspan, George P. Shultz, and John H. Cochrane

Summary of the Commentary

Ian J. Wright

Monday, August 27, 2012

Which Simple Rule for Monetary Policy?

The discussion of "Simple Rules for Monetary Policy" at last week’s FOMC meeting is a promising sign of a desire by some to return to a more rules-based policy. As described in the FOMC minutes, the discussion was about many of the questions raised in recent public speeches by FOMC members Janet Yellen and Bill Dudley. A big question is which simple rule?

Yellen and Dudley discussed two rules. Using Yellen’s notation these are

R = 2 + π + 0.5(π - 2) + 0.5Y

R = 2 + π + 0.5(π - 2) + 1.0Y

where R is the federal funds rate, π is the inflation rate, and Y is the GDP gap. Yellen and Dudley refer to the first equation as the Taylor 1993 Rule and the second equation as the Taylor 1999 Rule, though the second equation was only examined along with other rules, not proposed or endorsed, in a paper I published in 1999.

The two rules are similar in many ways. Both have the interest rate as the instrument of policy, rather than the money supply. Both are simple, having two and only two variables affecting policy decisions. Both have a positive weight on output. Both have a weight on inflation greater than one. Both have a target rate of inflation of 2 percent. Both have an equilibrium real interest rate of 2 percent.

The two rules differ substantially, however, in their interest rate recommendations as this amazing chart constructed last April by Bob DiClementi of Citigroup illustrates. The chart shows two rules along with historical and projected values of the federal funds rate. The rule labeled “Taylor” by DiClementi is the rule I proposed. The other rule is labeled “Yellen” by DiClementi because it corresponds to the rule apparently favored by Yellen. The projected values are the views of FOMC members.

Observe that the first rule never gets much below zero, while the second rule drops way below zero during the recent recession and delayed recovery. The difference continues though it gets smaller into the future. Note that the projected interest rates by FOMC members span the two rules.

Observe that the first rule never gets much below zero, while the second rule drops way below zero during the recent recession and delayed recovery. The difference continues though it gets smaller into the future. Note that the projected interest rates by FOMC members span the two rules.

This big difference between the two rules in the graph can be traced to two factors: (1) The second rule has a much larger GDP gap, at least as used by Yellen. (2) The second rule has a much bigger coefficient on the GDP gap.

In my view, a smaller value of the GDP gap and a smaller coefficient are more appropriate. This view is based on a survey of estimated gaps by the San Francisco Fed and simulations of models over the years. But given the striking differences in DiClememti's chart, more research on the issue by people in and out of the Fed would certainly be very useful.

Yellen and Dudley discussed two rules. Using Yellen’s notation these are

R = 2 + π + 0.5(π - 2) + 0.5Y

R = 2 + π + 0.5(π - 2) + 1.0Y

where R is the federal funds rate, π is the inflation rate, and Y is the GDP gap. Yellen and Dudley refer to the first equation as the Taylor 1993 Rule and the second equation as the Taylor 1999 Rule, though the second equation was only examined along with other rules, not proposed or endorsed, in a paper I published in 1999.

The two rules are similar in many ways. Both have the interest rate as the instrument of policy, rather than the money supply. Both are simple, having two and only two variables affecting policy decisions. Both have a positive weight on output. Both have a weight on inflation greater than one. Both have a target rate of inflation of 2 percent. Both have an equilibrium real interest rate of 2 percent.

The two rules differ substantially, however, in their interest rate recommendations as this amazing chart constructed last April by Bob DiClementi of Citigroup illustrates. The chart shows two rules along with historical and projected values of the federal funds rate. The rule labeled “Taylor” by DiClementi is the rule I proposed. The other rule is labeled “Yellen” by DiClementi because it corresponds to the rule apparently favored by Yellen. The projected values are the views of FOMC members.

This big difference between the two rules in the graph can be traced to two factors: (1) The second rule has a much larger GDP gap, at least as used by Yellen. (2) The second rule has a much bigger coefficient on the GDP gap.

In my view, a smaller value of the GDP gap and a smaller coefficient are more appropriate. This view is based on a survey of estimated gaps by the San Francisco Fed and simulations of models over the years. But given the striking differences in DiClememti's chart, more research on the issue by people in and out of the Fed would certainly be very useful.

Thursday, August 16, 2012

Democracy is Not a Spectator Sport, Even for Economists

It’s good news that economic issues are now getting more attention in the presidential campaign. More than 400 economists have signed a statement on the differences between the Romney economic program and the Obama program—the numbers are growing each day—and economic commentators including on CNBC and the Wall Street Journal (here and here) are discussing it. Judging by the hits on this post on Economics One, there’s a great deal of interest in the issues rasied in the economic white paper—authored by Kevin Hassett, Glenn Hubbard, Greg Mankiw and me—comparing the effects on economic growth of the Romney program and the Obama program. Of course, the selection of Paul Ryan has set off a huge number of articles on economics from budget policy to monetary policy.

It’s already clear to most voters that the presidential candidates have vastly different approaches to economic policy. But many people are still not informed about the implications of these two approaches. In my view the more voters get informed, and the more their votes are based on that information, the more likely the officials they elect will be able to revive the economy.

But this will not happen if the political campaign drifts back away from substance as campaigns so often do. Keeping the debate focused on economics requires that economists participate and not merely sit back and watch. To remind myself of this, I like to wear this "Democracy is not a spectator sport" tie a lot during the election season.

It’s already clear to most voters that the presidential candidates have vastly different approaches to economic policy. But many people are still not informed about the implications of these two approaches. In my view the more voters get informed, and the more their votes are based on that information, the more likely the officials they elect will be able to revive the economy.

But this will not happen if the political campaign drifts back away from substance as campaigns so often do. Keeping the debate focused on economics requires that economists participate and not merely sit back and watch. To remind myself of this, I like to wear this "Democracy is not a spectator sport" tie a lot during the election season.

Monday, August 13, 2012

Paul Krugman is Wrong

Paul Krugman took time off from his vacation last Friday to take a shot at a paper by Kevin Hassett, Glenn Hubbard, Greg Mankiw and John Taylor on the growth and employment impacts of Governor Romney’s economic program in comparison with President Obama’s program. Though flaming with vitriolic rhetoric, his shot misses the mark.

Half of Krugman’s piece strays away from the paper, so focus on what he actually says about the paper.

First, he says that that the “work of other economists” cited in the paper does not support its position. But the research papers and books that are cited are quoted correctly and do provide supporting evidence. As Scott Sumner reports “when I looked at the paper I couldn’t find a single place where they had misquoted anyone.” And Jim Pethokoukis shows not only that the evidence cited in the paper is supportive, but also that Krugman is on record as previously agreeing with the cited work on the 2009 stimulus package.

Second, Krugman claims that the authors whose work is cited in the paper have also done other work which is not supportive of other aspects of the paper. The example he mentions is the work of Atif Mian and Amir Sufi showing that the slump is “demand-driven” in addition to their cited work on the cash-for-clunkers program (and much other work by the way). But work showing that the slow recovery is demand-driven is not evidence that the Romney program will not increase economic growth. As the paper on the Romney economic program states, the program works in two ways: "It will speed up the recovery in the short run, and it will create stronger sustainable growth in the long run." Demand and supply are at work.

Third, Krugman asserts that the “Baker et al paper claiming to show that uncertainty is holding back recovery clearly identifies the relevant uncertainty as arising from things like the GOP’s brinksmanship over the debt ceiling — not things like Obamacare.” Well there is nothing about “the GOP’s brinkmanship” in the Baker et al paper; those are Krugman’s words. And the paper on the Romney economic program does not link Baker et al to Obamacare. The Baker et al paper uses an index of policy uncertainty which has been very high in recent years for many reasons including uncertainty about future taxes and the debt problem, as exemplified by the 2011 debt dispute, which had its origins prior to 2011, including in 2009 and 2010. That is exactly the point: Policy uncertainty is high now for a number of reasons, and reducing it with a long-term strategy rather than more short-term fixes will increase economic growth and create jobs.

Half of Krugman’s piece strays away from the paper, so focus on what he actually says about the paper.

First, he says that that the “work of other economists” cited in the paper does not support its position. But the research papers and books that are cited are quoted correctly and do provide supporting evidence. As Scott Sumner reports “when I looked at the paper I couldn’t find a single place where they had misquoted anyone.” And Jim Pethokoukis shows not only that the evidence cited in the paper is supportive, but also that Krugman is on record as previously agreeing with the cited work on the 2009 stimulus package.

Second, Krugman claims that the authors whose work is cited in the paper have also done other work which is not supportive of other aspects of the paper. The example he mentions is the work of Atif Mian and Amir Sufi showing that the slump is “demand-driven” in addition to their cited work on the cash-for-clunkers program (and much other work by the way). But work showing that the slow recovery is demand-driven is not evidence that the Romney program will not increase economic growth. As the paper on the Romney economic program states, the program works in two ways: "It will speed up the recovery in the short run, and it will create stronger sustainable growth in the long run." Demand and supply are at work.

Third, Krugman asserts that the “Baker et al paper claiming to show that uncertainty is holding back recovery clearly identifies the relevant uncertainty as arising from things like the GOP’s brinksmanship over the debt ceiling — not things like Obamacare.” Well there is nothing about “the GOP’s brinkmanship” in the Baker et al paper; those are Krugman’s words. And the paper on the Romney economic program does not link Baker et al to Obamacare. The Baker et al paper uses an index of policy uncertainty which has been very high in recent years for many reasons including uncertainty about future taxes and the debt problem, as exemplified by the 2011 debt dispute, which had its origins prior to 2011, including in 2009 and 2010. That is exactly the point: Policy uncertainty is high now for a number of reasons, and reducing it with a long-term strategy rather than more short-term fixes will increase economic growth and create jobs.

Friday, August 3, 2012

It’s Still a Recovery in Name Only--A Real Tragedy

I have been regularly charting the path of real GDP and employment during the recovery from the recession as new data are released. From the start it was clear that the recovery was very weak. By its second anniversary the recovery was weak for long enough to call it “a recovery in name only, so weak as to be nonexistent.” Now we are just past the third anniversary, and it is still at best a recovery in name only. It’s now the worst in American history—a tragedy that should not be minimalized.

Here’s an update of the charts using the latest data through the second quarter or through July for monthly data. The first one shows real GDP in this recovery. You can see that the gap between real GDP and potential GDP (CBO estimates) is not closing at all. That is the main reason why unemployment remains so high.

Second is the comparison chart with the recovery from the previous deep recession in the early 1980s.That is a typical recovery from a deep recession. The gap closes.

Some say that recoveries from deep U.S. recessions--or from financial crises--are usually slower, but this is simply not true. Below are similar charts from the 1893-94 recession

Of course potential GDP is difficult to measure so it is important to look at alternative charts. The next one used GDP growth rates. The average real GDP growth rate in this recovery has been only 2.2 percent, even lower than the 2.4 percent before the data were revised.

Tuesday, July 31, 2012

Still Learning from Milton Friedman

We can still learn much from Milton Friedman, who was born 100 years ago today. Here I focus on his role in the macroeconomic debates of the 1960s and 1970s, because they are so similar to the debates raging again today.

Friedman, Samuelson, and Rules Versus Discretion

First, go back to the early 1960s. The Keynesian school was coming to Washington led more than anyone else by Paul Samuelson who advised John F. Kennedy during the 1960 election campaign and recruited people like Walter Heller and James Tobin to serve on Kennedy’s Council of Economic Advisers. In fact, the Keynesian approach to macro policy received its official Washington introduction when Heller, Tobin, and their colleagues wrote the Kennedy Administration’s first Economic Report of the President, published in 1962.

The Report made an explicit case for discretion rather than rules: “Discretionary budget policy, e.g. changes in tax rates or expenditure programs, is indispensable…. In order to promote economic stability, the government should be able to change quickly tax rates or expenditure programs, and equally able to reverse its actions as circumstances change.” As for monetary policy a “discretionary policy is essential, sometimes to reinforce, sometimes to mitigate or overcome, the monetary consequences of short-run fluctuations of economic activity.”

In that same year Milton Friedman published Capitalism and Freedom (1962) giving the competing view on role of government which he then continued to espouse through the 1960s and beyond. He argued that “the available evidence . . . casts grave doubt on the possibility of producing any fine adjustments in economic activity by fine adjustments in monetary policy—at least in the present state of knowledge . . . There are thus serious limitations to the possibility of a discretionary monetary policy and much danger that such a policy may make matters worse rather than better . . . The basic difficulties and limitations of monetary policy apply with equal force to fiscal policy . . . Political pressures to ‘do something’ . . . are clearly very strong indeed in the existing state of public attitudes. The main moral to be had from these two preceding points is that yielding to these pressures may frequently do more harm than good. There is a saying that the best is often the enemy of the good, which seems highly relevant . . . The attempt to do more than we can will itself be a disturbance that may increase rather than reduce instability.”

Resolving the Disagreements

So there were two different views: the Samuelson view versus the Friedman view. The fundamental disagreement was not really over which instrument of government policy worked better (monetary versus fiscal), but rather over discretion versus rules-based policies. From the mid-1960s through the 1970s the Samuelson view was winning with practitioners putting many discretionary policies into practice.

But Friedman remained a persistent and resolute champion of his alternative view. At one time during the 1970s, F.A. Hayek even seemed to be siding with the discretionary approach, at least in the case of monetary policy. But Milton Friedman didn’t waver. In fact he sent a letter to Hayek in 1975 saying: “I hate to see you come out as you do here for what I believe to be one of the most fundamental violations of the rule of law that we have, namely discretionary activities of central bankers.” Fortunately, in my view, Friedman’s arguments eventually won the day and American economic policy moved away from such a heavy emphasis on discretion in the 1980s and 1990s.

The Debate Returns

But this same policy debate is back today. Economists on one side push for more discretionary fiscal stimulus packages. They argue that the stimulus packages of 2008 and 2009 either worked or should have been even larger. They also push for more discretionary monetary policy such as the quantitative easing actions. They are not so worried about discretionary bailout policy, discounting the increased moral hazard that lack of a credible rule implies. In these ways they are descendants of the Samuelson school.

Other economists argue for more stable fiscal policies based on permanent tax reforms and the automatic stabilizers. They also push for a return to more predictable and rule-like monetary policy.They argue that neither the discretionary fiscal stimulus packages nor the bouts of quantitative easing were very effective, pointing to the risks of increased debt or monetization of the debt. They worry about the consequences of the discretionary bailouts. In these respects they are descendants of the Friedman school.

Of course there are many nuances today, some related to the difficulty of distinguishing between rules and discretion. You can see this, for example, in discussions of nominal GDP targeting, where some see it as a rule and some see it as a license to proceed with whatever discretionary action it takes. Interestingly, you frequently hear people on both sides channeling Milton Friedman to make their case.

Resolving the Debate Again

While academics are still the main protagonists, the debate is not academic. Rather it is a debate of enormous practical consequence with the well-being of millions of people on the line. Can the disagreements be resolved? Milton tended toward optimism that they could be resolved, and I am sure that this is one reason why he kept researching and debating the issue so vigorously.

Here people on both sides can learn from him. First, while a vigorous debater he was respectful, avoiding personal attacks and never failing to answer a letter. Second, he had a strong believe that empirical evidence would bring people together. He was influenced by statistician Leonard (Jimmie) Savage: Yes, people would come to the issue with widely different prior beliefs, but their posterior beliefs—after evidence was collected and analyzed—would be much closer. In this way the disagreement would eventually be resolved. I think we saw this in the late 1970s and the basic agreements lasted for at least two decades.

Unfortunately, posterior beliefs in the macro area now seem just as far apart as prior beliefs were 50 years ago. Clearly we have a lot of work to do, and clearly we can learn a lot from Milton Friedman in deciding how to proceed.

Friedman, Samuelson, and Rules Versus Discretion

First, go back to the early 1960s. The Keynesian school was coming to Washington led more than anyone else by Paul Samuelson who advised John F. Kennedy during the 1960 election campaign and recruited people like Walter Heller and James Tobin to serve on Kennedy’s Council of Economic Advisers. In fact, the Keynesian approach to macro policy received its official Washington introduction when Heller, Tobin, and their colleagues wrote the Kennedy Administration’s first Economic Report of the President, published in 1962.

The Report made an explicit case for discretion rather than rules: “Discretionary budget policy, e.g. changes in tax rates or expenditure programs, is indispensable…. In order to promote economic stability, the government should be able to change quickly tax rates or expenditure programs, and equally able to reverse its actions as circumstances change.” As for monetary policy a “discretionary policy is essential, sometimes to reinforce, sometimes to mitigate or overcome, the monetary consequences of short-run fluctuations of economic activity.”

In that same year Milton Friedman published Capitalism and Freedom (1962) giving the competing view on role of government which he then continued to espouse through the 1960s and beyond. He argued that “the available evidence . . . casts grave doubt on the possibility of producing any fine adjustments in economic activity by fine adjustments in monetary policy—at least in the present state of knowledge . . . There are thus serious limitations to the possibility of a discretionary monetary policy and much danger that such a policy may make matters worse rather than better . . . The basic difficulties and limitations of monetary policy apply with equal force to fiscal policy . . . Political pressures to ‘do something’ . . . are clearly very strong indeed in the existing state of public attitudes. The main moral to be had from these two preceding points is that yielding to these pressures may frequently do more harm than good. There is a saying that the best is often the enemy of the good, which seems highly relevant . . . The attempt to do more than we can will itself be a disturbance that may increase rather than reduce instability.”

Resolving the Disagreements

So there were two different views: the Samuelson view versus the Friedman view. The fundamental disagreement was not really over which instrument of government policy worked better (monetary versus fiscal), but rather over discretion versus rules-based policies. From the mid-1960s through the 1970s the Samuelson view was winning with practitioners putting many discretionary policies into practice.

But Friedman remained a persistent and resolute champion of his alternative view. At one time during the 1970s, F.A. Hayek even seemed to be siding with the discretionary approach, at least in the case of monetary policy. But Milton Friedman didn’t waver. In fact he sent a letter to Hayek in 1975 saying: “I hate to see you come out as you do here for what I believe to be one of the most fundamental violations of the rule of law that we have, namely discretionary activities of central bankers.” Fortunately, in my view, Friedman’s arguments eventually won the day and American economic policy moved away from such a heavy emphasis on discretion in the 1980s and 1990s.

The Debate Returns

But this same policy debate is back today. Economists on one side push for more discretionary fiscal stimulus packages. They argue that the stimulus packages of 2008 and 2009 either worked or should have been even larger. They also push for more discretionary monetary policy such as the quantitative easing actions. They are not so worried about discretionary bailout policy, discounting the increased moral hazard that lack of a credible rule implies. In these ways they are descendants of the Samuelson school.

Other economists argue for more stable fiscal policies based on permanent tax reforms and the automatic stabilizers. They also push for a return to more predictable and rule-like monetary policy.They argue that neither the discretionary fiscal stimulus packages nor the bouts of quantitative easing were very effective, pointing to the risks of increased debt or monetization of the debt. They worry about the consequences of the discretionary bailouts. In these respects they are descendants of the Friedman school.

Of course there are many nuances today, some related to the difficulty of distinguishing between rules and discretion. You can see this, for example, in discussions of nominal GDP targeting, where some see it as a rule and some see it as a license to proceed with whatever discretionary action it takes. Interestingly, you frequently hear people on both sides channeling Milton Friedman to make their case.

Resolving the Debate Again

While academics are still the main protagonists, the debate is not academic. Rather it is a debate of enormous practical consequence with the well-being of millions of people on the line. Can the disagreements be resolved? Milton tended toward optimism that they could be resolved, and I am sure that this is one reason why he kept researching and debating the issue so vigorously.

Here people on both sides can learn from him. First, while a vigorous debater he was respectful, avoiding personal attacks and never failing to answer a letter. Second, he had a strong believe that empirical evidence would bring people together. He was influenced by statistician Leonard (Jimmie) Savage: Yes, people would come to the issue with widely different prior beliefs, but their posterior beliefs—after evidence was collected and analyzed—would be much closer. In this way the disagreement would eventually be resolved. I think we saw this in the late 1970s and the basic agreements lasted for at least two decades.

Unfortunately, posterior beliefs in the macro area now seem just as far apart as prior beliefs were 50 years ago. Clearly we have a lot of work to do, and clearly we can learn a lot from Milton Friedman in deciding how to proceed.

Thursday, July 26, 2012

Benefits of More Fed “Action” Do Not Exceed Costs

Both the New York Times and the Wall Street Journal ran front page stories yesterday reporting that the Fed is yet again about to take action. “Fragile Economy Said to Push Fed to Weigh Action” said the Times. “Fed Moves Closer to Action” said the Journal. Both stories report that the benefits of such actions in the past have exceeded the costs, but there is precious little evidence for this. In an interview in the latest issue of MONEY Magazine I was asked about this:

What’s your assessment of the Federal Reserve’s recent actions to help spur the economy? The Fed has engaged in extraordinarily loose monetary policy, including two round s of so-called quantitative easing. These large scale purchases of mortgages and Treasury debt were aimed at lifting the value of those securities, thereby bringing down interest rates. I believe quantitative easing has been ineffective at best, and potentially harmful.