In a report on fixed income, David Owen, Chief European Financial Economist at Jefferies, notes that demand for credit in Europe has plunged.

Owen asks

Is it the supply or demand for credit that matters?25 April 2012

Perhaps the most memorable comment Mario Draghi made to the European Parliament today was the need for a euro area Growth Pact, but he did draw comfort from the results of the ECB’s latest Bank Lending survey.

Draghi made reference to the fact that the balance of firms tightening credit conditions had fallen (from 35% in January to 9%). However, that it is not to say that credit conditions are actually easing, just that they are no longer tightening at the same rate as in January.

Not only are credit conditions still tightening, albeit at a slower rate, but importantly the ECB’s latest Bank Lending survey shows credit demand collapsing. This is not something that Mario Draghi mentioned to the European Parliament at all.

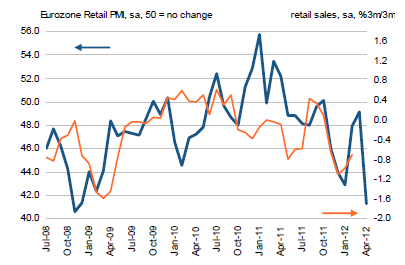

Europe Faces Japan SyndromeIn reference to the above chart, Ambrose Evans-Pritchard at

The Telegraph says

Europe faces Japan syndrome as credit demand implodesEurope (minus Germany) looks more like post-bubble Japan each month.

The long-feared credit crunch has mutated instead into a collapse in DEMAND for loans. Households and firms are comatose, or scared stiff, in a string of countries.

Demand for housing loans fell 70pc in Portugal, 44pc in Italy, and 42pc in the Netherlands in the first quarter of 2012. Enterprise loans fell 38pc in Italy. The survey took place in late March and early April, and therefore includes the second of Mario Draghi’s €1 trillion liquidity infusion (LTRO).

The ECB said net demand for loans had fallen "to a significantly lower level than had been expected in the fourth quarter of 2011, with the decline driven in particular by a further sharp drop in financing needs for fixed investment." Demand fell 43pc for household loans, and 30pc for non-bank firms.

This slump in loan demand is more or less what happened during Japan’s Lost Decade as Mr and Mrs Watanabe shunned debt. Zero interest rates did nothing. The Bank of Japan was "pushing on a string" (though it never really launched bond purchases with any serious determination).

The credit squeeze is entirely predictable – and was widely predicted – given that banks must raise their core Tier 1 capital ratios to 9pc by July to meet EU rules, or face nationalisation. (The pro-cyclical folly of this beggars belief: by all means impose higher buffers, but not during a recession, and not by letting banks slash their balance sheets. The US at least forced its banks to raise capital, an entirely different policy since it does not lead to a lending crunch.)

The IMF said last week that Europe’s banks would slash their balance sheets by €2 trillion – or 7pc – by next year. This amounts to an economic shock. The Fund said deleveraging on this scale at a time of sharp fiscal tightening risks a "bad equilibrium".

Or one analyst said, the LTRO lets northern banks dump their bond holdings onto Club Med banks. The renationalisation of the eurozone financial system goes a step further.

The LTRO "carry trade" is already revealing the sting in its tail in any case since the banks are by now underwater on a lot of bonds. What happens if and when they need to sell those bonds to cover debts falling due over the next year?

Until the ECB conducts monetary policy with proper energy, calls for "Growth Compacts" from governments amount to humbug. The ECB needs to do its own work.

We all know why it will not do so: because Hayekian romantics at the Bundesbank hold sway, and none of the other governors dare say boo. Live with the consequences.

Live with the Consequences IndeedPritchard conveniently ignores the fact that Japan is struggling right now to "live with the consequences" of numerous misguided monetary and fiscal stimulus efforts over 20 years. Japan has debt-to-GDP exceeding 200% and little to show for it. And Japan now has to live with the consequences of numerous misguided QE and stimulus proposals.

Pritchard apparently wants more QE for Europe as if that would increase demand for credit.

Note that two rounds of QE did not increase the demand for credit in the US as per my post

The Real Consumer Credit Story: Virtually No Recovery in Revolving Credit, No Recovery in Non-Revolving Credit.

Moreover, QE did not succeed in increasing the demand for credit in Japan over 20 years. So pray tell why would QE increase the demand for credit in Europe? More importantly, even if it did, would that be a good thing?

European banks are already over-leveraged and under-capitalized so how the hell is providing cheap credit going to possibly do anything good?

Would 0% interest rates help when that did not help Japan?

Pritchard Misses the BoatClearly Pritchard missed the boat on QE as well as the desirability of attempting to cram more credit down banks' throats when banks are over-leveraged and under-capitalized.

Everyone wants to do something "but not now". While there is immense merit to not hiking taxes in a recession as Brussels forced on Greece, Spain, and Portugal, work rule and pension changes are badly needed.

Pritchard's idea of raising capital instead of selling assets seems reasonable enough. However, nothing stops banks from doing that, at least in theory. Is practice another matter?

Giant Sucking Sound William Wright discusses Tier-1 Capital requirements in

A rough guide to surviving the great deleveraging of 2012As if Basel III weren’t enough of a headache, big European banks face a deadline of June 30 from the European Banking Authority to increase their core Tier-1 capital ratios to 9%, equivalent to raising €115bn in equity.

In theory, banks can meet this by retaining profits, raising equity or shrinking assets. But with equity markets all but closed to banks and earnings falling, a crash diet to reduce their bloated balance sheets is the only realistic option.

Analysts expect that the great bank deleveraging of 2012 could see as much as $2 trillion to $3 trillion of assets trimmed from European banks’ balance sheets – or about 5% of total assets – with damaging consequences not only for the banking industry but for the fragile European economy.

Here is a rough guide to some of the inevitable consequences – some deliberate, some unintended and some obscure – of this deleveraging on the investment banking industry.

Death of profits, jobs and banks

The most obvious impact of deleveraging will be the devastation it will wreak on the profits of investment banks. In 2006, Goldman Sachs posted a return on equity of 33% and its core leverage – assets divided by equity – was 29 times. Fast forward to the first nine months of this year, and its return on equity was 3.7% with leverage of 14 times. Not because it has radically shrunk its balance sheet (yet) but because it has more than doubled its equity.

The same process will play out across the industry, where the combination of an increase in the cost of business driven by regulation is colliding with a downturn in activity. This will choke off profits, with JP Morgan forecasting that average ROE for the industry will fall to just 8% next year. That’s in line with research by Financial News that shows average pretax ROE in the first nine months of this year was 12% (or about 8% net).

Structurally lower profitability has already prompted banks such as Credit Suisse and UBS to slash their fixed income trading activities. While the thousands of job cuts seem harsh, they are often in the low single digits in terms of overall headcount. As more banks grasp the nettle in 2012, they will pull out of entire business lines, cutting 10% or 20% of their staff – or pull out of investment banking altogether.

Is That All Bad News?Wright concludes that is not all bad news. I agree, but for some different reasons.

First Wright ...

The Promised Land

In all of this, there is some good news. For those banks that can survive the rigours of deleveraging without having to pull out of entire regions or businesses while retaining a profitable operation, there is a Promised Land on the other side. Overcapacity in the investment banking industry will be whittled away to leave a smaller number of bigger and (relatively) more profitable global banks whose scale will increasingly play to their advantage.

Bankers talk of JP Morgan, Deutsche Bank, Goldman Sachs and perhaps one other – maybe Bank of America Merrill Lynch, Barclays Capital or Citi – emerging stronger than ever. At the same time there will be a larger number of product and sector specialists, which will drop the “me-too” approach of the past decade.

In this new world, with a realistic price for risk and credit and less competition, margins can only go one way: up.

Banks Should Be Banks, Not Hedge FundsI do not believe that bigger is better and I am sick of the notion "too big to fail". Indeed, it most often means two things:

- Too Big To Succeed

- Taxpayer Bailouts

Banks should be banks, not hedge funds. To the extent that Basel III forces banks to shed trading activities and other non-traditional activities that banks now find themselves in, I view that as a good thing.

I certainly agree with Wright regarding the need for "a realistic price for risk and credit", but "less competition" is certainly not the essence of well-formed free markets.

My conclusion is that Wright does not understand the Fed's role in the creation of this mess or sound Austrian economic principles needed to fix it.

We will indeed see a "a realistic price for risk and credit" if and only if we get rid of the Fed and end fractional reserve lending. Bigger banks are not the answer.

By the way, Wright is not quite correct when he says "

equity markets all but closed to banks".

Let's phrase the idea properly: "

equity markets all but closed to banks, on terms that banks want". Banks do not want shareholder dilution that comes with raising equity now.

Bondholders do not want to take a hit either. Both should have happened already. However, Bush, Obama, Congress, and the Fed acted in unison to prevent what desperately needed to happen.

If Not Now, When?Pritchard thinks the time to raise Tier-1 Capital requirements is not now. OK, when is it? 10 years from now? Or will Spain, Greece, and Italy still be too fragile?

Japan shows the folly of depending on QE and fiscal stimulus to spawn inflation, then waiting for it to happen.

Japan's Four-Pronged Approach - Fiscal Stimulus

- Monetary Stimulus (QE)

- Misguided Hope

- Ignore Capital Impairments of Banks Waiting for Things to Get Better

Did Japan succeed?

In the case of Europe, there is also this "not-so-little" problem that Pritchard is extremely aware of yet mysteriously avoids every time he rails about the ECB not doing enough. I am obviously talking about the Euro.

The LTRO increased leverage and risk on Spanish and Italian banks. QE is useless, something Pritchard should see. Reducing interest rates will shift imbalances to other countries, and may send oil and food prices higher, but it sure will not increase lending.

Pritchard says "

The ECB needs to do its own work, with proper energy." What "work" is that? Does any "work" make any sense?

The first irony is Pritchard compares Europe to Japan, while essentially proposing the same four-pronged policy of failure followed by Japan.

The second irony of Pritchard's column is that if Basel III moves forward the date of the inevitable breakup of the eurozone, that would be a good thing. A eurozone breakup would place Europe on a faster pace of ending the very "Japan Syndrome" that Pritchard rails against.

Proper EnergyNot only do I want to raise tier-1 capital requirements, I want to see a 100% gold-backed dollar, the end of fractional reserve lending, and the end of duration-mismatched lending (e.g. selling 5-year CDs and making mortgage loans for 30 years).

Finally, lending of money that is supposed to be available on demand is fraudulent and must be stopped. I would be more than willing to phase those ideas in, but the time to start is now, not 10 years from now under the misguided notion things will be better if only banks would lend more.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List